UK construction output increases at sharper rate but outlook deteriorates

Story by

November 9, 2018

UK construction companies indicated a sustained increase in business activity during October. The overall rate of expansion improved slightly since September and was the second-strongest in 16 months. This mainly reflected a rebound in civil engineering activity, however, as both residential and commercial activity increased more slowly. Less positively, new projects rose only modestly, and firms were the least optimistic regarding growth prospects in nearly six years.

UK construction companies indicated a sustained increase in business activity during October. The overall rate of expansion improved slightly since September and was the second-strongest in 16 months. This mainly reflected a rebound in civil engineering activity, however, as both residential and commercial activity increased more slowly. Less positively, new projects rose only modestly, and firms were the least optimistic regarding growth prospects in nearly six years.

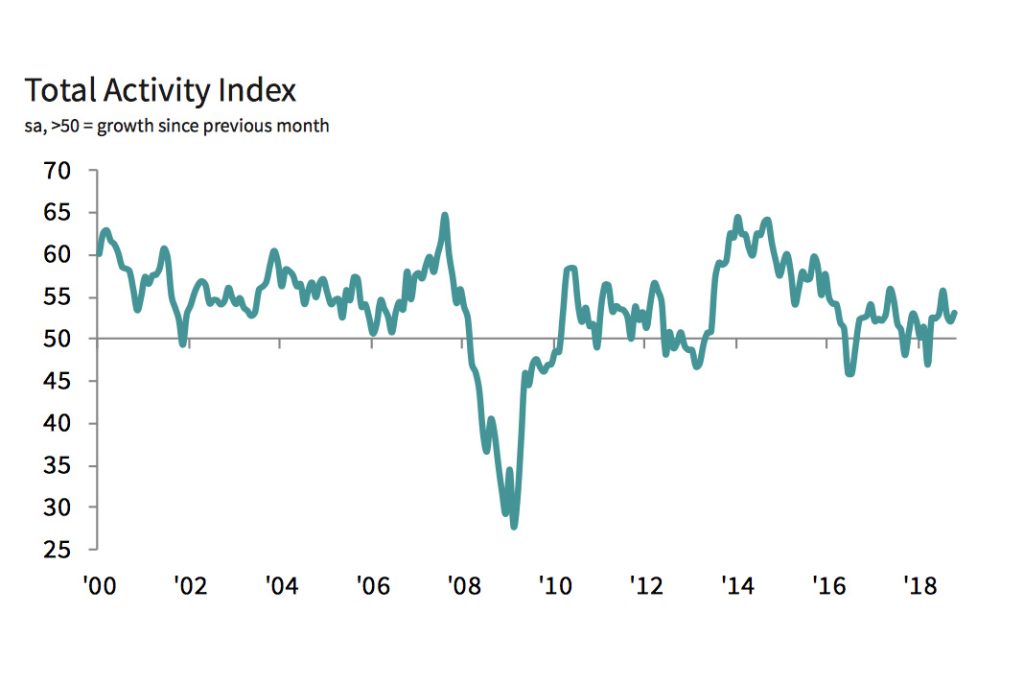

At 53.2 in October, up from 52.1 in September, the seasonally-adjusted IHS Markit/CIPS UK Construction Total Activity Index posted its second-highest level in 16 months. That said, it was still below the long-run survey average of 54.3. Construction output has risen every month since April. Higher activity was linked to the commencement of new contracts, overseas work and a general increase in business.

Of the three broad categories monitored, civil engineering drove the overall uptick in the rate of growth in October. Having declined in both August and September, activity in the sector rose at the strongest pace since July 2017 at the start of the final quarter. Meanwhile, housebuilding and commercial construction both increased at solid rates in October, albeit the weakest in seven and five months respectively. Consequently, civil engineering was the best- performing segment for the first time since January.

In contrast to the trend seen for construction activity, latest data pointed to a slower rise in new business volumes. The rate of new contract growth was the weakest in the current five-month sequence of expansion. Some firms mentioned intense competition in the market and delayed final decisions from clients.

Slower new order growth impacted firms’ expectations for future growth, with the business expectations index falling to a near six-year low. Alongside muted new project intakes, firms highlighted uncertainty related to Brexit and the economy as undermining confidence.

In response to the slowdown in growth of incoming new projects, construction companies increased their input purchasing more cautiously. The overall volume of inputs purchased continued to rise in October, but at the slowest rate in seven months. More positively, firms continued to increase employment at a strong overall rate.

Despite the softer rise in inputs being ordered, delivery times for construction products and materials continued to lengthen markedly in October. Firms continued to report stock shortages at vendors.

Cost pressures in the UK construction sector remained strong in October, despite the rate of input price inflation easing to a 27-month low. Firms highlighted increased fuel, labour, timber and steel costs. Sub-contractor rates also continued to rise at a relatively strong pace during the month.

Trevor Balchin, economics director at IHS Markit, which compiles the survey: “Although total UK construction activity rose at a stronger pace in October, the underlying survey data paint a less rosy picture for the sector towards the end of the year.

“New contracts increased at only a modest pace, and firms were the least optimistic regarding the 12-month outlook for nearly six years. Construction companies again linked uncertainty to Brexit negotiations, which influenced delays to final decisions at clients.

“Moreover, the higher total activity figure reflected the civil engineering sector, which saw a rebound following declines in August and September. Housing and commercial construction activity both rose more slowly in October, and at rates that remained below long-run survey averages.

“More positively, construction firms continued to raise headcounts at a strong pace, suggesting they are not expecting an imminent contraction in demand. That said, if the new orders and expectations indices remain at current levels or fall further, the employment index could also drift back towards the 50.0 no-change mark.”

Duncan Brock, group director at the Chartered Institute of Procurement & Supply: “On the surface, the construction sector showed growth but there was plenty for businesses to be concerned about underneath.

“Optimism was at its lowest level for six years, as the sector remained stifled by client hesitation, fears about the health of the UK economy and continued Brexit uncertainty, resulting in slower growth of new orders and purchasing.

“However, job creation bucked this downward trend with one of the highest levels of hiring in the last three years and civil engineering experienced a slight reprieve after a few disappointing months. The slowdown in the housing sector as the main driver of recent growth was unsurprising given the poor performance in UK house sales.

“These results point to the sector getting stuck in the mud as we approach March 2019, and with ongoing supplier delays and stock shortages, the sector may not be able to respond quickly enough anyway should there by a sudden upturn in fortunes.”